The $240M SaaS Nobody's Watching: Inside Commerce.com ($CMRC)

The $240M SaaS Nobody's Watching: Inside Commerce.com ($CMRC)The company formerly known as BigCommerce just quietly turned cash-flow positive — while its stock fell 65%. Here's what the market may be missing, and the risks that keep me from pounding the table.

The 30-second take: CMRC trades at $2.91 — roughly 0.70x sales for a business growing the top line in the low-single digits but with rapidly shrinking losses and real free cash flow. It’s cheap for a reason (decelerating growth, brutal competition from Shopify), but the risk/reward is more interesting than the chart suggests. Here’s the full picture — both sides — so you can decide for yourself. What this company actually isIf the ticker CMRC threw you, you’re not alone. On August 1, 2025, BigCommerce Holdings rebranded to Commerce.com, Inc. and swapped its ticker from BIGC to CMRC. Same business, new wrapper. Commerce.com is an open SaaS commerce platform — think of it as the enterprise-friendly alternative to Shopify — and it’s now the parent of three brands: the core BigCommerce storefront engine, Feedonomics (product-feed and marketplace data management), and Makeswift (visual page building). The pitch is “open SaaS”: rather than locking merchants into one walled garden, Commerce.com sells a composable, API-first stack that mid-market and enterprise retailers bolt onto existing systems. It’s a real, audited, Nasdaq-listed software company headquartered in Austin — not a shell, not a meme. And at a sub-$250M market cap, it’s squarely in our wheelhouse. How Commerce.com actually makes moneyTo underwrite a name like this, you have to understand the revenue engine — not just the headline. Commerce.com runs a multi-tenant, subscription-led SaaS model with two broad customer tiers. Enterprise plans target large retailers doing $50M+ in annual online sales and are sold on negotiated, usage-and-feature-tiered contracts; this is where the company has deliberately pushed upmarket over the last several years to chase larger, stickier accounts. Essentials plans (Standard, Plus, Pro) serve mid-market and smaller merchants on more standardized monthly pricing. Layered on top of the core storefront subscription are two growth levers that matter to the bull case. Feedonomics manages product data feeds and syndication to marketplaces like Amazon, Google, and Meta — a high-retention, mission-critical service that expands the company’s wallet share per merchant and is less commoditized than basic hosting. Makeswift adds visual, no-code page building that keeps marketing teams inside the platform. The strategic logic is straightforward: move from “we host your store” to “we run your entire commerce data and experience layer,” which raises switching costs and supports the 78.7% gross margin. The reason the upmarket shift matters for our thesis is mix. Enterprise revenue tends to be larger-contract, multi-year, and higher-retention — which is exactly what you want when top-line growth is slowing, because it makes the remaining growth more durable and more predictable. The flip side, and the bears’ counter, is that enterprise sales cycles are long and lumpy, and a 2.8% growth year suggests the upmarket motion isn’t yet offsetting churn and slower new-logo adds at the lower end. Both things can be true at once. The chart that tells the story

This is the part that makes value-minded readers lean in. The stock has fallen roughly 65% over two years, from about $8.38 in June 2024 to $2.91 today. The 52-week range alone runs from $2.41 to $5.54 — meaning you’re buying near the lower end of where it’s traded all year. On the day I pulled this data, shares were down 8.49%, so this is a name actively being thrown out, not one that’s already re-rated. Here’s the senior-analyst framing I’d put on a one-pager: when a profitless-growth story gets repriced as a no-growth value story, the bar to surprise is low. CMRC doesn’t need to reaccelerate to 20% growth to work from here. It needs to keep doing what the financials below already show it’s doing. The numbers: slow growth, but a real turnaround in profitability

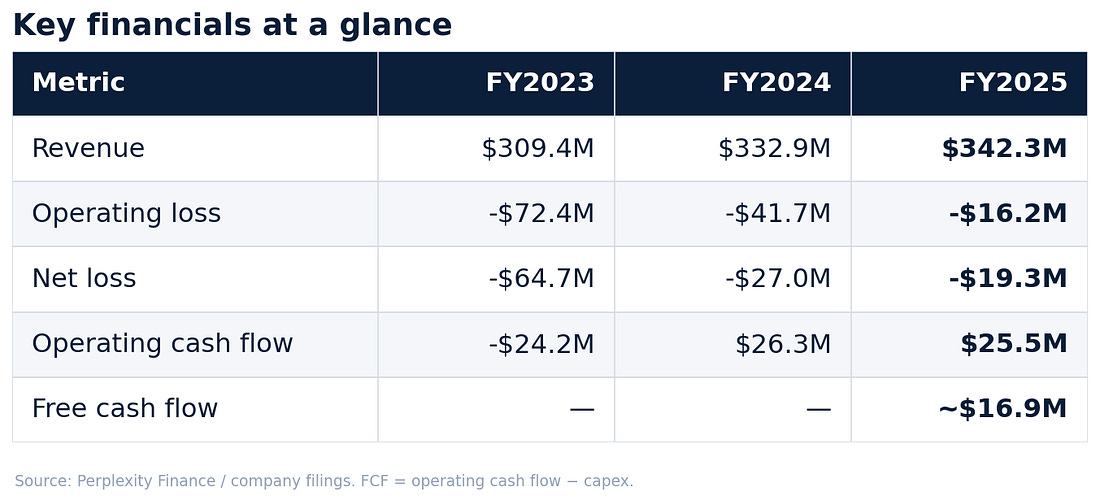

Revenue reached $342.3M in FY2025, up 2.8% year over year — a clear deceleration from the 7.6% growth posted in FY2024. That’s the bear’s first exhibit, and it’s legitimate: this is not a fast grower anymore. But look at the red line. Operating losses have collapsed from -$72.4M in FY2023 to -$41.7M in FY2024 to just -$16.2M in FY2025. Net loss followed the same path: -$64.7M → -$27.0M → -$19.3M. Management cut its way to the edge of GAAP profitability without gutting the product — R&D was still $73.0M in FY2025. The metric that matters most for a stock this cheap is cash. Operating cash flow swung from -$24.2M in FY2023 to a positive $25.5M in FY2025. After capex, that’s roughly $16.9M of free cash flow — a 4.9% FCF margin. Gross margin is a healthy 78.7%, which is exactly the kind of software economics that makes operating leverage possible as the company scales. The balance sheet backs the turnaround: $141.1M in cash and short-term investments against $39.4M of book equity, and no traditional total-debt figure reported. In plain English: this company is not going to be forced into a dilutive raise at a bad price. It can fund itself.

Valuation: this is the whole argumentAt $2.91 and a $240M market cap on $342.3M of revenue, CMRC trades at roughly 0.70x sales. For context, healthy SaaS businesses with 78% gross margins routinely command 4–8x sales. Even Shopify, the 800-pound gorilla, trades at a massive premium to this. You are paying value-stock multiples for a software company that is finally generating cash. On forward earnings, consensus has CMRC swinging to a profit: estimated EPS of $0.25 in FY2026 and $0.41 in FY2027, on revenue of about $355.2M next year and roughly $30.8M of free cash flow. That puts the stock at about 11.7x forward FY2026 earnings — cheap for any profitable software name. The trailing picture is still negative (TTM EPS of -$0.19), so this is explicitly a “the turn is happening” thesis, not a “it already turned” one. What Wall Street thinks (and why they can’t agree)

This is one of the most divided analyst setups I follow. Across 4 covering analysts, it’s a dead split: 2 bullish, 2 bearish, for a “Hold” consensus. The average price target is $5.12 — about 76% above today’s price — but the dispersion is enormous. Needham’s Scott Berg carries a $7.50 Buy (roughly 158% upside), while Barclays’ Raimo Lenschow sits at an Underweight $3.00 (basically flat from here, about 3% upside). Morgan Stanley downgraded to Underweight at $4 in January 2026. When targets range from $3.00 to $7.50 on the same stock, it tells you the outcome hinges almost entirely on one variable: does growth stabilize, or keep sliding? The honest scorecard✅ The bull case (pros)

⚠️ The bear case (cons)

What I’m watching from hereFor readers who want to track this alongside me, here are the specific signposts that would move my read in either direction. I’d rather give you a checklist than a hot take. Bullish triggers (would push me toward outright constructive): (1) two consecutive quarters of revenue growth stabilizing or reaccelerating above the ~3% FY2025 pace; (2) the first clean GAAP-profitable quarter, validating the consensus FY2026 EPS of $0.25; (3) evidence that Feedonomics and any agentic/AI-commerce products are driving net revenue retention higher; (4) a continued march of free cash flow above the ~$16.9M FY2025 level toward the ~$30.8M the Street models for FY2026. Bearish triggers (would make me step aside): (1) revenue actually declining year over year, which would confirm the bears’ “no-growth” framing; (2) a reacceleration in losses or a swing back to cash burn; (3) stock-based comp staying stubbornly near 7% of revenue, meaning per-share value leaks even as the business improves; (4) any sign Shopify or Adobe Commerce is taking enterprise logos directly from Commerce.com. The beauty — and the danger — of a 0.70x-sales stock is that expectations are already on the floor. The market is paying for stagnation, and “merely stable” would likely be enough to re-rate the shares. But the growth ceiling and the Shopify shadow are real, and worth sizing around. Putting it togetherHere’s how I’d frame the setup without telling you what to do with it. This is a business decelerating to ~3% growth in a Shopify-dominated market — that’s a real ceiling, and the bears aren’t wrong to be cautious. At the same time, at 0.70x sales with $141M in net cash, a balance sheet that removes solvency risk, and a profitability inflection that’s already showing up in cash flow, the downside looks more protected than the chart implies, while the upside (if growth merely stabilizes and the AI-commerce optionality plays out) could be meaningful. The average analyst target of $5.12 implies ~76% upside; even the skeptics’ floor near $3.00 is roughly where it trades today. This is a classic cheap-software setup: the market has priced in permanent stagnation, and the open question is simply whether that’s correct. Watch the next two quarterly prints for any sign of revenue stabilization — that’s the single variable that decides whether this re-rates toward $5 or stays stuck near $3. Where you land on it is your call. ⚖️ IMPORTANT DISCLAIMER — PLEASE READ This newsletter is for informational and educational purposes only and represents the personal opinions of the author. It is not investment, financial, legal, or tax advice, and nothing here is a recommendation, solicitation, or offer to buy or sell any security. Micro- and small-cap stocks like $CMRC are highly volatile, can be thinly traded, and may result in the total loss of your investment. The author and/or affiliated parties may hold positions in securities mentioned and may buy or sell them at any time without notice. All data is sourced from third-party providers believed to be reliable as of the publication date but is not guaranteed to be accurate, complete, or current; figures may be revised. Past performance and analyst price targets are not indicative of future results. Always do your own research and consult a licensed financial advisor before making any investment decision. By reading this, you agree that the author and publisher bear no liability for any losses or damages arising from your use of this information. You're currently a free subscriber to Cheap Software Stocks. For the full experience, upgrade your subscription.

|