Salesforce Just Set a Record No One Wanted

Salesforce Just Set a Record No One WantedA neutral, data-first breakdown of the most-hated blue-chip in software. No price target. No recommendation. Just the facts, so you can decide.

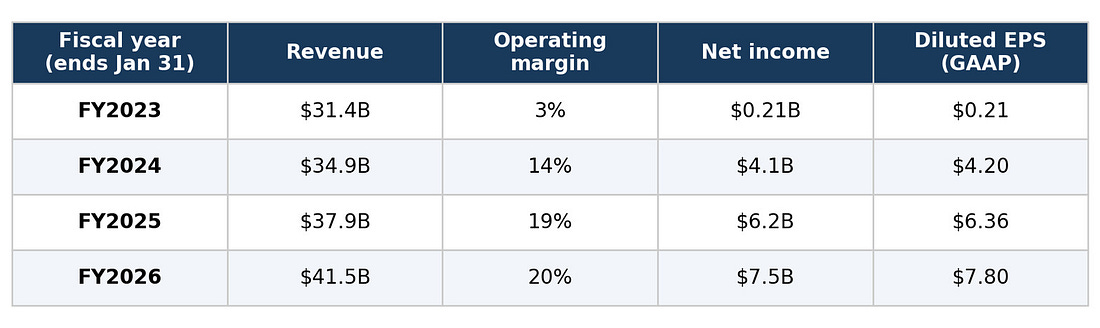

The setupThrough the Monday, June 22, 2026 close, Salesforce ($CRM) had fallen for 14 consecutive trading sessions — every session since June 1. According to data compiled by MarketWatch and Morningstar, that is the longest losing streak on record in the company’s history as a public company. Our own analysis of Salesforce’s full daily price record (more than 5,000 trading days back to 2006) confirms it: the prior record was eight straight down days, set only a handful of times. Fourteen stands alone. (If the stock declines again in any session after this close, the streak simply lengthens — the record is already broken either way.) Over that streak the stock fell from a June 1 close of $209.60 to $150.12 — a decline of roughly 28% in three weeks. It now sits roughly 46% below its 52-week high of $276.80, near the low end of its 52-week range ($147.58). On an intraday basis it touched its lowest levels since early 2023. A losing streak, by itself, tells you nothing about where the stock goes next. It is a measure of sentiment and positioning, not of value. What follows is the underlying business and balance-sheet picture — the things that actually determine whether the current price is an opportunity, a value trap, or simply fair. What the business actually looks likeStrip away the tape, and this is not a broken company. It is a large, profitable, cash-generative software franchise growing in the high single digits.

Two things stand out:

Cash generation is the strongest part of the picture. In FY2026 Salesforce produced $15.0B in operating cash flow. Consensus estimates put FY2027 free cash flow near $14.9B. Capital returns: aggressive, and now debt-fundedThis is where the story gets more nuanced, and where reasonable investors disagree. In FY2026, Salesforce spent $12.6B on share buybacks and $1.6B on dividends. In February 2026 the board authorized a new, record $50 billion repurchase program. In the most recent quarter the company launched a $25 billion accelerated repurchase — half the authorization — and, critically, it is funding that $25B portion with new debt. The bull reading: management believes the stock is materially undervalued and is using a depressed price plus cheap-relative-to-equity debt to retire shares aggressively. The buybacks helped reduce diluted share count and support EPS. The bear reading, which must be stated honestly: funding buybacks with debt is a material shift in financial policy. The rating agencies noticed. Moody’s downgraded Salesforce one notch to A2, and S&P revised its outlook to negative, both citing the increased leverage. A buyback only creates value if the shares are genuinely cheap and the core business is intact; if the business is deteriorating, debt-funded buybacks can mask the decline rather than reverse it. That is a legitimate risk, not a hypothetical. A note on share count: over the FY2023–FY2026 span, diluted weighted-average shares fell only about 4% (from ~997M to ~956M), because stock-based compensation issuance partly offset repurchases. The more aggressive reduction is recent, tied to the FY2026 and accelerated programs. What insiders are doingInsider activity is one of the cleaner signals available, so it’s worth being precise. Over the last 18 months (Jan 2025 – May 2026), across roughly 1,176 filed transactions:

How to read this fairly: heavy insider selling at a large-cap is largely routine — executives diversify, and much of it is pre-scheduled (10b5-1 plans) or tied to option exercises and vesting. It is weak evidence of a bearish view. The buying is more informative because open-market purchases are discretionary and rare. A handful of directors put real personal money in — some near $260, well above the current $150 (i.e., they are underwater), and some near $194 in March (also above it). There has been no disclosed open-market insider buying at current levels in this dataset. Net: modest, scattered insider conviction on the buy side, dwarfed in dollar terms by routine executive selling. Earnings: a quietly improving track recordThe most recent quarter was a clear beat. For Q1 FY2027 (reported May 27, 2026), Salesforce posted EPS of $3.88 versus a consensus near $3.12 (a beat of roughly $0.76) and revenue of $11.13B, ahead of the ~$11.05B estimate. Notably, the stock still fell ~0.8% the day after — a sign the market’s concern is about the future (AI disruption, growth) more than the present (current results). The prior several quarters show a mixed pattern on the headline EPS line (several apparent “misses” against consensus in FY2026), but those comparisons are muddied by GAAP-vs-adjusted definitional differences and one-time items. Revenue has been steadier, generally landing at or slightly above consensus. The takeaway: execution on the top line has been consistent; the debate is about durability, not about whether the company is hitting near-term numbers. Valuation: be careful which “P/E” you useThis is the single most important thing to get right, because it’s where most takes go wrong.

Honest framing: on trailing GAAP earnings, ~17.4x is not extraordinarily cheap for a high-single-digit grower — it’s roughly a market multiple. On adjusted earnings and free cash flow, the stock looks cheaper, and that’s the lens the bulls (and most sell-side analysts) use. Both are valid; they are simply different yardsticks. The dividend yield is negligible (~0.01%, effectively a rounding error against the share price), so this is a buyback-and-growth story, not an income story. What Wall Street thinksAmong the 28 analysts with current ratings, 20 are bullish, 7 neutral, 1 bearish — a consensus “Buy.” But the dispersion is enormous and is the real story:

Even the lowest published target ($173) is above the current $150. That tells you the sell-side broadly views the stock as oversold relative to their models — but the spread from $173 to $400 also tells you there is no consensus on what this business is worth, which is exactly what you’d expect for a company whose terminal value hinges on an unresolved question. The actual debate, in one paragraph eachThe bull case (neutral statement of it): A profitable, $41.5B-revenue franchise generating ~$15B in annual cash flow, still growing ~9%, with expanding margins, trading ~46% off its high near multi-year lows. Management is so convinced it’s cheap that it authorized a $50B buyback and is taking on debt to accelerate it. It’s using the downturn to acquire AI capabilities — most notably a definitive agreement, signed June 15, 2026, to buy Fin (formerly Intercom) for ~$3.6 billion (expected to close around early 2027), alongside earlier-2026 deals for m3ter and Contentful — all to fold into its Agentforce agent platform. If Agentforce reaccelerates growth, today’s price looks like a gift. The bear case (neutral statement of it): Growth has decelerated from hypergrowth to mature-growth and could slow further. The entire premise of seat-based enterprise software is under question if AI agents reduce the number of human “seats” companies need — and Salesforce’s own Agentforce push is an implicit acknowledgment of that threat. The debt-funded buyback drew a Moody’s downgrade and an S&P negative outlook, and could be masking deterioration rather than creating value (the IBM-in-the-2010s comparison). On trailing GAAP earnings (~17.4x) the stock is not screamingly cheap, and “cheap” only holds on adjusted metrics that exclude real costs like stock comp. The bottom lineThe facts are not in dispute: Salesforce just set a record losing streak, it is deeply out of favor, it is highly profitable and cash-generative, it is buying back stock aggressively with borrowed money, and its core business model faces a genuine, unresolved question about AI. Whether that adds up to a buy depends entirely on one judgment call you have to make yourself: do you believe AI is a tailwind that Salesforce can harness (Agentforce, the Fin acquisition), or a headwind that erodes its seat-based core faster than margins and buybacks can compensate? The numbers can frame that question with precision. They cannot answer it for you. Sources: company financial statements (FY2023–FY2026), consensus analyst data, Form 4 insider filings, and quoted market data as of the June 22, 2026 close. Acquisition, buyback, and credit-rating details corroborated by CNBC, MarketWatch, Morningstar, Reuters/Irish Times, and rating-agency commentary (Moody’s, S&P).

You're currently a free subscriber to Cheap Software Stocks. For the full experience, upgrade your subscription.

|