The Most Hated Blue-Chip in Software

Autodesk is one of the most misunderstood large-cap software companies trading today. While the stock sits near 52-week lows — down roughly 30% from its 2021 peak and lagging the broader software recovery — the underlying business has never been stronger. The company just delivered its best quarter in three years, accounting scandals have been fully resolved with no restatement and closed government investigations, a transformational go-to-market restructuring is ahead of schedule, and free cash flow surged 54% year-over-year to $2.4 billion in fiscal year 2026. The market is penalizing ADSK for near-term disruption from a sales force restructuring while ignoring the structural margin expansion story unfolding in real time. This is a classic case of Wall Street confusing short-term friction with long-term impairment. We believe ADSK deserves a 43%+ rerating from current levels over the next 12-18 months — and that is a conservative base case. This is not a momentum bet. It is a value and quality compounding story in one of the most defensible software franchises on earth. What Autodesk Actually Does — And Why It MattersAutodesk has been building software for people who design and make things since 1982. AutoCAD, the company’s flagship product, became the standard drafting tool for architects, engineers, and designers globally over four decades. That dominance is not nostalgia — it is an installed base moat that takes a generation to dislodge. The company now serves four primary verticals through a cloud-first subscription platform:

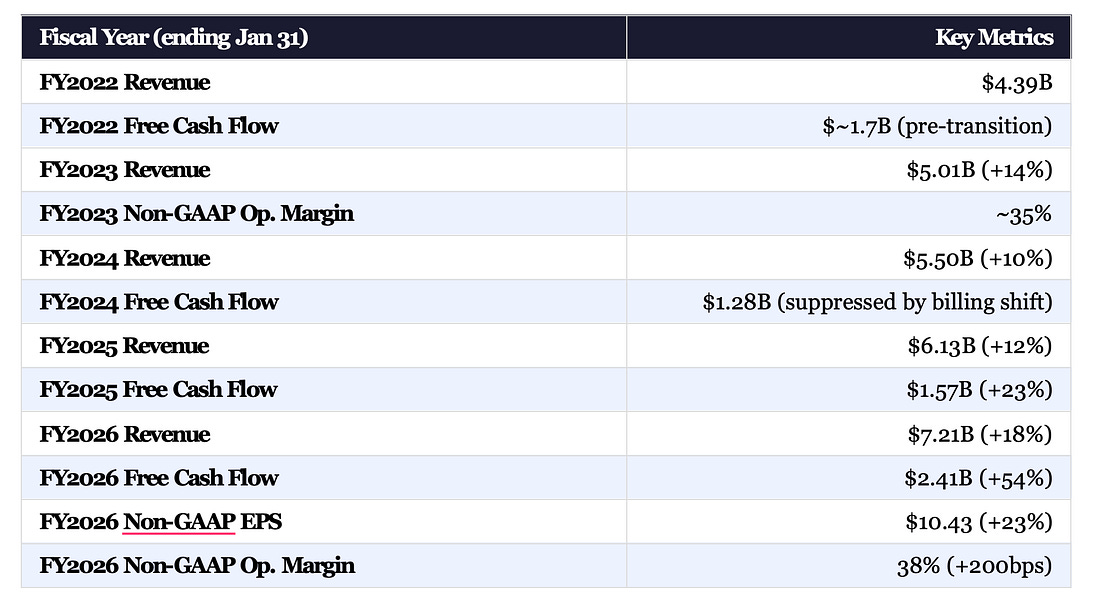

The genius of the business model transformation completed over the past five years is this: Autodesk converted virtually its entire revenue base from perpetual licenses to cloud subscriptions. Today, 97% of revenue is recurring. The customer is locked in not through contractual force but through workflow integration — thousands of project files, templates, trained teams, and supply chain integrations built on Autodesk’s formats. You don’t switch away from that on a Tuesday. The Financial Transformation: Four Years of EvidenceThe numbers tell a story of deliberate, sustained compounding. Here is the progression across four annual reports:

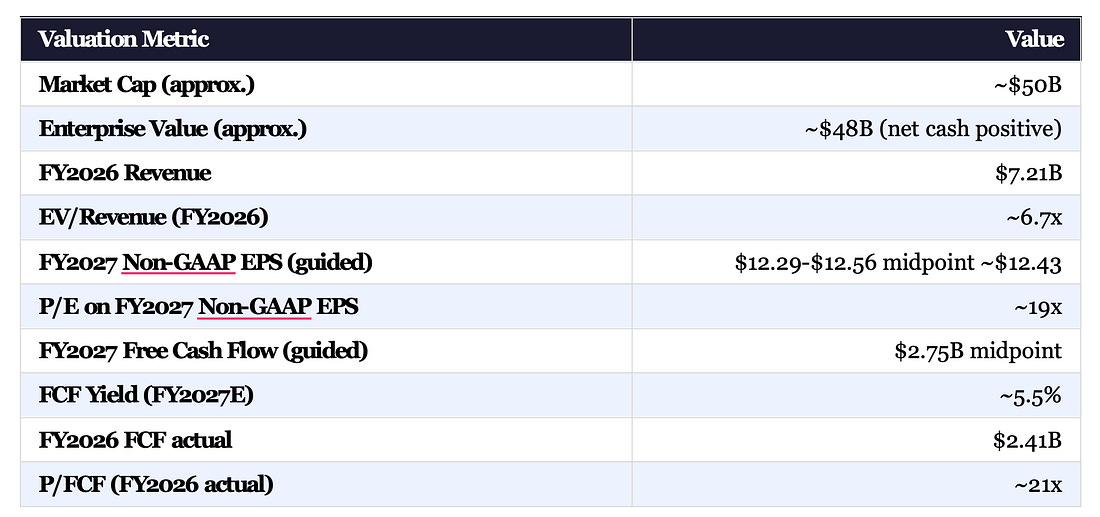

That 54% free cash flow surge in FY26 is the headline number that the market has not yet priced. It is not a one-time event — it reflects the normalization of billing patterns after a multi-year transition from upfront multi-year contracts to annual billing, and the first wave of margin expansion from go-to-market restructuring. The FY27 FCF guidance of $2.7-2.8B represents another 15%+ increase. Subscriptions grew to 7.79 million in FY25, up ~516K year-over-year. Remaining Performance Obligations (RPO) hit $8.3 billion in Q4 FY26, up 20% year-over-year, with current RPO of $5.5B. That is nine months of forward revenue visibility already contracted. Businesses do not build this kind of backlog unless customers are deeply committed. The Elephant in the Room: The Accounting Investigation — And Why It’s OverIn April 2024, Autodesk disclosed an internal investigation into its free cash flow and non-GAAP operating margin practices. The stock fell sharply. The SEC and the U.S. Department of Justice for the Northern District of California both opened inquiries. Activist investor Starboard Value, which held over $500 million in ADSK shares, issued a scathing letter accusing management of manipulating metrics. Here is what actually happened, and why the overhang has fully cleared: The investigation found that management had, during FY2022 and FY2023, pushed enterprise customers toward multi-year upfront billing arrangements to help meet free cash flow targets — a practice that was disclosed in aggregate terms but not quantified. Management also timed certain discretionary spending and collections to influence reported free cash flow. This was poor governance and sloppy disclosure, but it was not accounting fraud. No revenue was fabricated. No expenses were hidden permanently. No restatement was required. The CFO who oversaw the period (Deborah Clifford) was reassigned to a strategy role, then ultimately departed. In August 2025, both the SEC and the USAO formally closed their investigations with no charges and no penalties. The case is over. The new CFO, Janesh Moorjani, who joined in December 2024 after a distinguished career at VMware and Nutanix, has explicitly flagged margin expansion as his primary mandate. His credibility is clean. The governance remediation has been completed. The class action lawsuits remain in early stages but are unlikely to represent material economic liability given the SEC/DOJ outcomes. What the market did: it de-rated the stock on the investigation and never fully re-rated it on the resolution. That is the opportunity. The New Transaction Model: Transition Friction Masking Structural UpsideBetween FY2024 and FY2026, Autodesk executed a fundamental overhaul of how it transacts with customers — shifting from an indirect channel model where resellers and distributors handled billing, to a direct billing model where Autodesk invoices customers directly (the ‘new transaction model’). This created significant noise in reported metrics: Billings were inflated during the rollout as the new model brought forward revenue recognition. GAAP revenue was temporarily elevated. And the percent of revenue through indirect channels fell from 63% in FY2024 to approximately 53% by FY2026 completion. The distortions made year-over-year comparisons nearly impossible to read cleanly. As of Q4 FY2026, the new transaction model rollout is complete in all markets. By Q2 FY2027, the comparison period will also reflect the new model, eliminating the distortion entirely. This is the clarifying moment for investors. The underlying business, stripped of transition noise, is growing revenue at 8-10% organically and expanding margins aggressively. The strategic benefits of direct billing are not cosmetic. Autodesk now has complete visibility into its end-customer base, pricing, and usage patterns for the first time in its history. This enables far more precise upselling, better renewal management, and — critically — the potential for consumption-based pricing models tied to AI usage. That option did not exist before. The Margin Expansion Story: Best in the Industry Is the TargetThis is the most underappreciated part of the thesis. Autodesk’s current non-GAAP operating margin of 38% sounds reasonable for a software company, but it is dramatically below what the business is structurally capable of. Compare to peers: ServiceNow operates at ~44% non-GAAP operating margins. Cadence Design Systems runs at ~40%+. Oracle’s cloud business generates margins above 50%. Adobe generates 45%+ non-GAAP margins. Autodesk’s 38% reflects a business that has been investing heavily in cloud infrastructure, platform development, and a go-to-market model that had significant duplication between direct and channel layers. Management has now explicitly guided to ‘GAAP margins among the best in the industry’ as the terminal target. For FY2027, GAAP operating margin guidance is 26-28% — a 400-600 basis point improvement over FY2026’s 22%. Non-GAAP operating margin guidance is 38.5-39%, up from 38%. The restructuring completed in FY2025/FY2026 (approximately 9% of workforce across two tranches — ~1,350 in February 2025 and ~1,000 in early 2026) eliminated significant redundancy in customer success, marketing operations, and sales overlayers. The savings are flowing directly to operating leverage, not back into headcount. Management plans to host an investor day in H2 FY2027 to lay out the full long-term margin roadmap. We believe this will be a catalyst. Our model suggests non-GAAP operating margins of 42-44% are achievable by FY2029, which on $9B+ of revenue would imply $3.8-4.0B of non-GAAP operating income and $3.5B+ of free cash flow. The Growth Engines: Construction Cloud and AIAutodesk Construction Cloud (ACC) Construction is the biggest TAM expansion story in the company’s history. The global construction industry — a $13 trillion sector — has historically been one of the least digitized industries on earth. Productivity growth in construction has lagged every other major industry for 50 years. Autodesk’s ACC suite (Autodesk Build, BuildingConnected, BIM Collaborate Pro, Takeoff, Cost, and the recently acquired Rhumbix) is attacking this directly. Make revenue — which captures ACC cloud subscriptions — grew 22% in FY2026 to $796M, accelerating from 25% in FY2025. This is the fastest-growing product family and now represents over 11% of total revenue, up from essentially zero in FY2020. The construction segment added nearly 400 net new logos in a single quarter. Major wins like Power Design and Cleveland Construction (displacing competitive solutions) demonstrate that Autodesk is now winning displacement deals, not just greenfield. The ACC platform strategy creates compounding switching costs. A general contractor using Autodesk Build for project management, BIM Collaborate Pro for design coordination, BuildingConnected for preconstruction bidding, and GCPay for payments has their entire project life cycle on Autodesk’s platform. Moving that stack is a multi-year organizational transformation. The NRR holding in the 100-110% range despite macro headwinds in construction is evidence of this stickiness. Project Bernini and the AI Opportunity Autodesk’s AI strategy is not about chatbots layered on top of existing products. It is about fundamental workflow automation built on proprietary training data accumulated over 40 years of customers submitting projects through Autodesk’s cloud infrastructure. Project Bernini — Autodesk’s generative 3D AI model — is the most visible piece of this. Bernini enables non-technical users to generate manufacturable 3D designs from text or 2D inputs, dramatically expanding the addressable user base beyond trained CAD professionals. The Fusion product’s AutoConstrain tool, which uses AI to suggest geometry constraints, has achieved a roughly 50% acceptance rate — meaning it is saving meaningful time on tasks that previously required manual expertise. More importantly, Autodesk’s CFO confirmed in early 2026 that the company is developing additional foundation models trained on customer datasets that are delivering ‘stronger and more cost-effective results’ than general-purpose AI models for Autodesk’s specific domains. This is a key differentiation: generic AI cannot match domain-specific models trained on millions of real construction plans, manufacturing drawings, and architectural designs. The monetization model for AI is still evolving, but the Flex consumption platform — token-based pay-as-you-go access — gives Autodesk a natural mechanism to charge for AI usage above base subscription tiers. As AI tools drive higher usage frequency and broader adoption, we expect Flex to become a material revenue contributor by FY2029. The Moat: Four Concentric Rings of DefenseAutodesk’s competitive position is sometimes underestimated because the company has faced perpetual competitive threats — from Dassault, Bentley, PTC, and more recently Trimble — without losing meaningful market position. Here is why: 1. The Installed Base / File Format Lock-In AutoCAD’s .DWG file format is the de facto standard for construction and engineering documentation. Hundreds of millions of drawings exist in this format. Every AEC firm has decades of project archives in DWG. Even if an architect wanted to switch to a competitor, their supplier chain — contractors, consultants, fabricators — uses Autodesk formats. This is a network effect disguised as a file format. 2. The Education Moat Autodesk provides free software to over 100 million students and educators through its Education Community. The IIT Bombay memorandum of understanding signed in Q4 FY2025 is one example of hundreds of university partnerships globally. Engineers graduate knowing Autodesk products, firms hire them, and the cycle perpetuates. Competitors cannot buy this; it took 40 years to build. 3. The Enterprise Data Moat The transition to cloud subscription has given Autodesk something it never had before: complete visibility into how customers use its products. Every click, every workflow, every collaboration event is now data. This enables AI training, predictive renewal analytics, and targeted upsell that competitors with legacy perpetual-license models simply cannot replicate. 4. The Platform Ecosystem The Autodesk Platform Services (APS, formerly Forge) connects over 3,000 third-party developers building on Autodesk’s APIs. This creates a flywheel: more integrations make Autodesk more valuable, more value attracts more developers, and the ecosystem becomes its own switching cost. Bentley and Trimble have nothing comparable in construction. Valuation: Cheap Relative to Quality and GrowthAt approximately $237 per share and a market cap of roughly $50 billion, here is how ADSK stacks up:

A 19x forward non-GAAP P/E for a business growing free cash flow at 15-20% annually, with 97% recurring revenue, an 8.3B RPO backlog, dominant market share in structural growth markets, and AI optionality is genuinely cheap. For comparison: ServiceNow trades at 45-50x forward non-GAAP earnings. Salesforce trades at 28-30x. Workday trades at 28x. Even Cadence and Synopsys — slower-growth EDA companies — trade at 35-40x. The consensus analyst price target is approximately $340-$360, representing 43-52% upside from current levels. We find the bull case — $380-400 — entirely reasonable if the FY2027 margin expansion plays out as guided and the AI narrative gets attached. Our base case price target of $340 represents approximately 27x FY2027 non-GAAP EPS of $12.43. This is a modest premium to the market multiple for a company of this quality growing FCF at mid-teens annually. Even applying a 25x multiple — a discount to peers — implies a target above $310. The Bull Case: $380 Upside scenario assumes: FY2027 margins beat guidance at 40%+, AI monetization begins to show up in billings growth re-acceleration, and construction recovery in Europe and the U.S. drives AECO above 25% growth. Multiple re-rates to 30x FY2027 non-GAAP EPS. The Bear Case: $210 Downside scenario assumes: Sales force restructuring creates more disruption than expected, new transaction model causes customer attrition, macro deterioration in construction markets pressures net new logos, and margins disappoint. At $210, the stock trades at roughly 17x FY2027 non-GAAP EPS — implying the market views this as a zero-growth utility, which is not credible given the construction cloud trajectory. What the Market Is Missing: The Five Mispricing Factors1. The FCF Normalization is Being Misread as a One-Time Benefit The 54% FCF surge in FY2026 is correctly attributed in part to the new transaction model bringing forward cash collections. But the base business FCF — stripping that out — is also growing 20%+ as margins expand. The market is discounting FY2027’s $2.75B FCF guidance as unsustainable. We believe it is the floor, not the ceiling. 2. The SEC/DOJ Closure is Underpriced Both government investigations closed in August 2025 with zero penalties. The psychological discount applied during the investigation period never fully unwound. Investors who were burned by the disclosure are still on the sidelines. That is not rational capital allocation — it is recency bias creating an opportunity. 3. The Go-to-Market Disruption is Temporary and Self-Inflicted Management explicitly guided for ‘temporary risk to billings and revenue’ as it operationalizes the sales optimization plan. This is management being unusually transparent about short-term headwinds. The stock is being punished for that transparency. The restructuring is designed to create a leaner, more productive sales organization. The disruption window is 2-4 quarters, not permanent. 4. Construction Cloud is Not Yet in the Model Most equity models still treat ADSK as primarily a Design software company with ACC as an emerging add-on. ACC is now $796M and growing at 22%+. In three years, it will represent 20%+ of revenue at premium SaaS multiples. The embedded optionality is enormous. 5. AI Will Create a New Monetization Layer Autodesk is uniquely positioned for AI because it has 40 years of proprietary design data, a specific technical domain where generic LLMs fail (3D geometry, manufacturing tolerances, construction codes), and a Flex consumption platform ready to monetize incremental AI usage. This optionality is valued at approximately zero in the current stock price. Risks Worth WatchingConstruction Market Cyclicality Autodesk’s AECO business is partially exposed to construction starts. A deeper-than-expected construction downturn driven by sustained high interest rates could slow net new logos and put pressure on renewal rates. Management’s NRR metric (currently 100-110%) is the canary in the coal mine here. Go-to-Market Disruption The second phase of the sales optimization plan — channel partner integration and digital self-service buildout — has not yet started. If it is botched, it could create multi-quarter revenue disruption. The departure of the CRO during the restructuring adds integration risk. AI Disruption Risk The longer-term question: could AI design tools from NVIDIA, Google, or specialized startups displace Autodesk workflows over a 5-10 year horizon? We think the answer is no — for the same reason it has not happened yet. Design and engineering is not a generalist AI task; it requires domain expertise embedded in proprietary models that Autodesk is actively building. But this is a risk that needs monitoring. Macro Sensitivity ADSK is global — 44% of revenue from international markets. Currency headwinds (the new transaction model somewhat amplifies FX exposure), geopolitical disruption, and a global construction slowdown could all pressure results. The company has not paid a dividend and does buybacks at a modest pace relative to FCF, limiting the yield cushion in a down market. The Bottom Line: A Tier-1 Software Franchise at a Tier-3 MultipleAutodesk is the standard-bearer for design and construction software globally. Its competitive position — built on 40 years of installed base, educational programs, and increasingly on cloud data and AI — is as defensible as any in enterprise software. The business has successfully transformed from a legacy perpetual license model to a 97% recurring revenue, cloud-first subscription business. Free cash flow is growing at 20%+ annually. Margins are expanding toward best-in-class. The regulatory overhang is fully resolved. And the stock trades at 19x next year’s non-GAAP earnings. We have reviewed four annual reports, every quarterly earnings call from the past two years, the investor day presentations, and all available sell-side research. The consensus is Buy with a $340-360 target. Our view is that the consensus is right for the wrong reasons — most models are not fully capturing the margin expansion potential, the ACC growth trajectory, or the AI monetization optionality. The stock is sitting near the bottom of its 52-week range ($215-$329), below its 200-day moving average, and at its lowest non-GAAP P/E multiple in years. When accounting scandals close, restructuring disruptions end, and FCF normalization becomes visible in real-time numbers, the stock re-rates. That process has already begun — ADSK rose 6% on its February 2026 earnings release. We are in the early innings. ADSK is a BUY. Price target $340. Time horizon 12-18 months. Disclosure & Disclaimer This article is for informational and educational purposes only and does not constitute investment advice. The author may hold positions in securities discussed. All financial data sourced from SEC filings, company press releases, and publicly available research. Past performance is not indicative of future results. Always conduct your own due diligence and consult with a qualified financial advisor before making investment decisions. Price data as of early April 2026. You're currently a free subscriber to Cheap Software Stocks. For the full experience, upgrade your subscription.

|