PayPal at 9x Earnings: The Most Misunderstood Setup in Large-Cap Fintech

PayPal at 9x Earnings: The Most Misunderstood Setup in Large-Cap FintechA new CEO with $25M tied to the stock price. A buyback program retiring 13% of shares per year. A business that throws off $6 billion of free cash flow. And a stock the market has left for dead.

PayPal trades at roughly $50 per share as of late April 2026. The stock is down more than 80% from its 2021 peak of $310. The trailing P/E sits around 9.3. The forward P/E is just under 10. For context, the ten-year average P/E is north of 28, and the 2020 high was nearly 80x. The current multiple is roughly 77% below the long-term historical average. This is what a fallen growth stock looks like when the market has stopped believing the growth story. But here’s what makes PYPL interesting at this price: even after assuming the growth thesis is dead, the math on capital returns alone is striking. The company is generating roughly $6 billion of free cash flow on a market cap of about $46 billion — a ~13% FCF yield — and returning essentially all of it to shareholders through buybacks and a newly initiated dividend. If you bought at today’s price and the business simply held flat for five years, you’d own a meaningfully larger slice of a still-profitable cash machine. That’s the entire thesis in one sentence. The question is whether “holds flat” is realistic. And the answer to that question depends almost entirely on a leadership team that just got rebuilt from the top. How we got here: the five-year fallTo understand why PayPal trades where it does, you need the brief history. PayPal was a pandemic darling. From the start of 2020 to mid-2021, the stock more than tripled to $310. The narrative was that COVID was permanently accelerating e-commerce, that PayPal would be the default checkout for a digitized world, and that Venmo would eventually be monetized into a second growth engine. Active accounts surged. Total payment volume surged. The company guided to 750 million active accounts by 2025, more than double its eventual peak. Then everything broke at once. E-commerce growth normalized as physical stores reopened. The 750 million target was quietly abandoned, then explicitly retracted. PayPal admitted it had been adding low-quality, incentivized accounts that didn’t transact. Take rates began compressing because the fastest-growing piece of the business — Braintree, the unbranded card processing operation that powers checkout for Uber, DoorDash, and others — operates at a fraction of the margin of branded checkout. Apple Pay went from a niche product to a default behavior on every iPhone. Shop Pay processed more volume each quarter than seemed possible. Stripe Link began offering one-click checkout that didn’t require the consumer to ever see PayPal. Three CEOs have now tried to fix this. Dan Schulman, who ran PayPal from the 2015 eBay spin-off through 2023, leaned into growth at any cost during the pandemic and then struggled to pivot. He was replaced in September 2023 by Alex Chriss, an Intuit veteran hired specifically to refocus the company on profitable growth. Chriss had a coherent plan: deprioritize low-margin Braintree, reinvigorate branded checkout, launch a one-click product called Fastlane to compete with Apple Pay, monetize Venmo via the debit card, and restart the buyback machine. He delivered on the capital returns immediately — $6 billion of buybacks in 2024 — but the operational turnaround was slower than the board’s patience allowed. In Q4 2025, branded checkout volume growth — the single most important metric in the entire company — decelerated to 1%, down from 7% a year earlier. The board fired Chriss on February 2, 2026. CFO Jamie Miller stepped in as interim. On March 1, 2026, Enrique Lores — the outgoing CEO of HP Inc. and a five-year PayPal board member — took the chair. This is where the current investment opportunity begins. The new management teamIf you’re going to underwrite a turnaround, you need to underwrite the people running it. The current bench is genuinely strong, and the comp structure tells you exactly what they’re being paid to do. Enrique Lores, President and CEOLores spent more than 30 years at HP, the last six as CEO. His track record is built on three things: he architected the separation of HP and HPE in 2015 to improve agility, he simplified HP’s cost structure during a brutal period for PCs and printing, and he delivered six consecutive quarters of revenue growth in a business everyone had written off as a melting ice cube. He pushed HP into subscriptions, services, and AI-enabled hardware while protecting cash generation. Importantly, he is not new to PayPal. He has been on the PayPal board for five years and served as Chair of the board. He didn’t need a learning ramp on the strategic issues; he was in the room when the previous CEO presented the plans that didn’t work. That dual experience — sitting in board meetings hearing what wasn’t getting done, and now being the person who has to do it — is unusual and useful. His public messaging since taking the seat has been careful and revealing: “execute with greater speed and precision,” “hold ourselves accountable for consistent delivery quarter on quarter,” “prioritize what matters most, simplify where necessary.” This is operator vocabulary, not visionary vocabulary. After three years of strategic narratives that didn’t translate to results, that shift in tone is welcome. He has already committed $400 million in 2026 to revamp the branded checkout experience. Jamie Miller, CFO and COOMiller is the kind of CFO you want during a turnaround. She joined PayPal in November 2023 after serving as Global CFO of EY, where she led the separation and aborted IPO of EY’s consulting arm. Before that she was CFO of Cargill, and before that she spent more than a decade at GE — including as CFO of the entire company and CEO of GE Transportation. She also currently sits on Qualcomm’s board. Her remit at PayPal expanded in 2025 to include the COO role, which is a strong signal the board was already grooming her for broader operational responsibility. When Chriss was fired, she was the natural interim choice, and she remains the operational backbone underneath Lores. She received a $3 million cash retention award to stay through the transition — which tells you the board considers her departure a real risk and is paying to prevent it. Miller has spent her career inside complex, multi-segment industrial businesses. PayPal — with its branded checkout, Braintree, Venmo, BNPL, merchant services, and emerging stablecoin/AI offerings — is exactly that kind of business. What Lores is being paidThe comp structure is, in my view, the single most underappreciated piece of this story. Here’s the package, pulled directly from the 8-K and proxy:

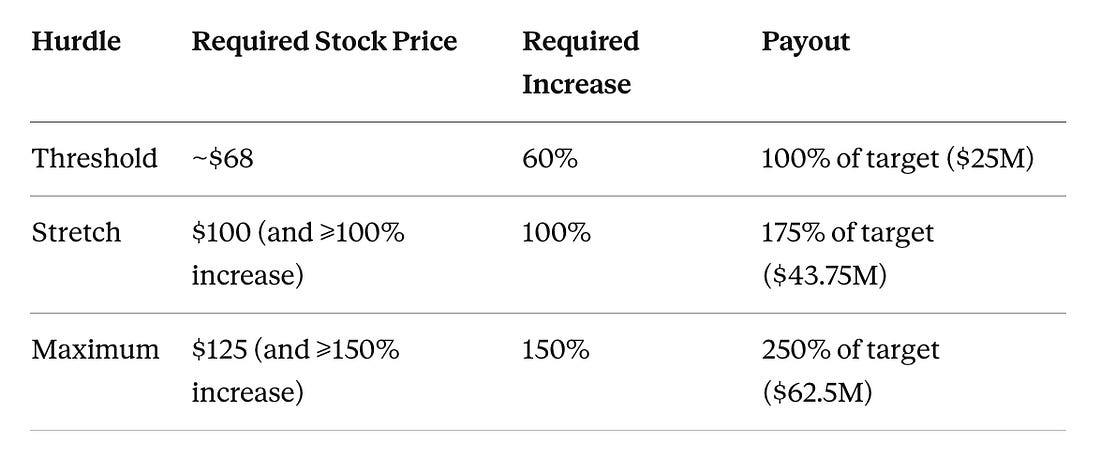

That last piece is the one that matters. The Stock Price PSU is the cleanest alignment instrument I’ve seen on a major turnaround in a long time. Here are the actual hurdles, against a baseline stock price of $42.58:

These are measured on the average closing price over any consecutive 60-calendar-day period, ending between the third and fifth anniversary of his March 1, 2026 start date. So between March 2029 and March 2031. Translate that into plain English: Lores does not get a meaningful chunk of his pay unless the stock at least gets back to where it was at the end of 2024. He doesn’t get the stretch payout unless PYPL more than doubles. He doesn’t get the maximum unless it nearly triples. He has $20M of “make-whole” RSUs that are essentially guaranteed, which is fair compensation for leaving HP. But the upside — the part that turns a $5M-a-year executive package into a $50M+ outcome — is entirely tied to a stock that needs to roughly double from where the package was struck. The proxy itself flags this design intent: “highly performance-oriented, with no sign-on cash component, and with a special performance-based equity award tied to rigorous stock price hurdles over a period up to five years.” When you’re trying to figure out whether a CEO actually believes in his business, look at how he’s paid. Lores is structurally short the stock if PayPal trades sideways for five years. He only wins if shareholders win first. That is exactly the alignment you want. The Chriss exitFor completeness: Chriss received severance under PayPal’s standard “termination without cause” plan and remains an employee in a non-officer capacity through March 2, 2026, to assist with the transition. There was no scandal, no clawback, no acrimony in the public filings — just a board that decided execution wasn’t fast enough and acted accordingly. The fact that Chriss is staying through the handoff (and that Miller is being paid to stay) suggests the transition is being run cooperatively rather than chaotically. What actually broke (and is it fixable?)To understand the opportunity, you have to understand the wound. The wound is branded checkout. Branded checkout is the yellow PayPal button you see on millions of e-commerce sites. When a consumer clicks it instead of typing in a card, PayPal earns a meaningfully higher take rate than it does on its other businesses. Mizuho’s Dan Dolev put it bluntly: the yield on the branded button is multiples of any other product in the portfolio. That button is in trouble. Here is the deceleration over the last five quarters:

This is the chart that got Chriss fired. The bear interpretation is straightforward: Apple Pay, Google Pay, and Shop Pay are systematically eating PayPal’s lunch, especially on mobile, and especially with younger consumers who never built the muscle memory of clicking the yellow button. In the U.S., PayPal’s user base is forecast to grow less than 1% in 2026 to roughly 92 million, while Apple Pay closes in on 90.5 million and Google Pay reaches 55 million. Stripe Link is doing similar damage on the merchant side. And agentic AI commerce — bots that complete purchases on your behalf — could bypass the checkout button entirely over a 5-10 year horizon. That’s the structural decline thesis. It isn’t crazy. Several analysts downgraded the stock after Q4 2025, citing exactly this view. Canaccord cut to Hold, arguing PayPal’s “core e-commerce proposition is losing relevance.” HSBC cut to Hold, citing low confidence in the company’s ability to stabilize branded volumes. Mizuho flagged that “the competitive nature of payments now appears more intense than we realized.” Now the bull interpretation. There are real reasons to believe the deceleration is partially fixable:

The honest version of the operational picture: branded checkout is 50% structurally challenged and 50% fixable with better product execution. We won’t know the split for 18-24 months. The investment question is whether the rest of the thesis works while we wait. The capital returns engineThis is where PayPal becomes genuinely interesting at $50, regardless of what you think about branded checkout.

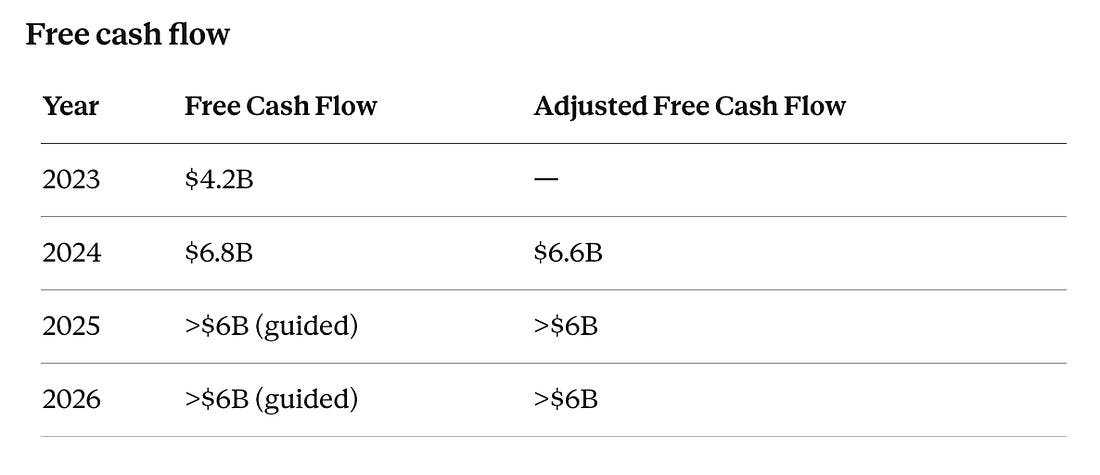

The business throws off cash. That hasn’t been in dispute through the entire deceleration. The bear case requires you to believe FCF is going to fall meaningfully — and even most bears don’t model a sharp decline before 2027-2028. BuybacksThis is the headline number. In 2024, PayPal returned $6 billion to shareholders by repurchasing approximately 92 million shares, reducing the average share count by roughly 6%. The board authorized a fresh $15 billion repurchase program alongside the Q4 2024 results, on top of $4.86 billion still remaining from the prior 2022 authorization. So roughly $20 billion of authorized buyback capacity at the start of 2025. In 2025, the company executed another $6 billion of buybacks, retiring approximately 84 million shares on a trailing-12-month basis as of mid-year. Management has guided to another $6 billion of buybacks in 2026. At today’s market cap of ~$46 billion, a $6 billion annual buyback is roughly 13% of shares outstanding being retired every year. There is no other large-cap fintech doing this. The shares-outstanding count tells the story:

That’s a 14% reduction in share count in 24 months. If the program continues at this pace through 2028, share count would approach 600 million — a one-third reduction from today. DividendPayPal initiated a quarterly dividend of $0.14 per share in 2025, the first in its history as a standalone public company. That’s roughly $500 million annually and a 1.1% forward yield at the current price. Modest in isolation, but symbolically important: the company is now committed to returning cash via two channels, not one, and management has indicated long-term targets of distributing 70-80% of FCF to shareholders annually. Balance sheetApproximately $14.8 billion in cash and investments against $11.6 billion in debt. Net cash positive. There is no leverage problem. The buyback can continue at $6 billion annually for years without requiring a single additional dollar of operating cash flow. The credit rating is investment grade and management has explicitly committed to maintaining it. Putting it togetherIf you own PayPal at $50, here is what is happening to your ownership stake mechanically, assuming the buyback continues at the guided pace:

Compounded, after three years, you own roughly 33% more of the company than you did at purchase. If FCF holds flat at $6B, your FCF per share goes from $6.50 today to $9.70. If the multiple holds at 9x, the stock is at $87. If the multiple expands modestly to 12x — still well below the historical average — the stock is at $116. Both outcomes assume the operational story does nothing to help. This is what people mean when they say a stock is “cheap.” Cheap doesn’t mean low absolute price. Cheap means the math works even when the narrative doesn’t. Long-term targets management has actually committed toThe 2025 proxy laid out explicit medium-term targets that are still operative under Lores. These are worth knowing because they frame the stock-price hurdles in his comp package:

If Lores delivers even the lower end of these targets, the stock should approach his $68 threshold hurdle without breaking a sweat. If he delivers the upper end, $100 stretch is in play. The targets and the comp package are pointed at the same outcome. That is rare. Most management comp packages are decoupled from public targets in ways that make them functionally meaningless. This one is designed to align. The valuation case, three waysThe simple way. Market cap ~$46B. Free cash flow ~$6B. That’s a 13% FCF yield on a business with a net cash balance sheet, a global brand with 438 million active accounts, and a CEO with a credible turnaround track record. Even if FCF declines 20% over five years, you’re still earning a yield well above the market. The buyback math. If PayPal repurchases $6B annually at an average price of $55 over the next three years, the share count drops from ~920M today to roughly ~600M by year-end 2028. If FCF holds flat at $6B, FCF per share goes from ~$6.50 today to ~$10. At even a 10x multiple, that’s $100/share — a double from here, with no help from the operational turnaround. This is, not coincidentally, exactly the stretch hurdle in Lores’ comp package. The operational re-rating. If Lores executes anything close to his HP playbook and branded checkout stabilizes at 4-5% growth — half of what it was at the end of 2024 — non-GAAP EPS could compound at low-to-mid teens over three years. The 2025 plan called for $4.95 to $5.10 in 2025 EPS; if 2028 EPS reaches $7.00 and the multiple expands from 9x to 13x (still below the 10-year average), the stock approaches $90-95. Add the buyback effect on share count and you can see how $100 becomes the base case rather than the bull case. The base case and bull case rhyme because the buyback does so much of the work. The bear case requires the buyback to actually break, which requires the cash flow to break, which requires multiple parts of the business to deteriorate simultaneously while a CEO with a strong track record fails to course-correct. That’s possible. It’s not the most likely path. The catalystThere are four catalysts worth watching in 2026: 1. May 5, 2026: Q1 earnings. This is Lores’ first quarter — even though he only took the seat March 1, the print and the call will be his first major message to the market. New CEOs almost always kitchen-sink and reset. Expect conservative full-year guidance, possibly an explicit reset of branded checkout expectations, and a clearer articulation of the 2026 reinvestment plan. Sentiment is so bad that simply stabilizing branded checkout growth at 1-2% would be received as good news. 2. Lores’ first strategic update (likely Q2 or Q3). New CEOs typically announce a strategic plan within their first 90-120 days. The HP playbook he ran was unsexy and effective: simplify, focus, cut cost, reinvest selectively, return cash. Apply that to PayPal and you get a credible 18-month story. Watch for explicit deprioritization of any product areas — Lores is famous for being willing to cut things, which is something Chriss was reportedly slower to do. 3. Branded checkout inflection. The $400M reinvestment is going into the checkout experience, biometric/passkey adoption (currently around 36%), and merchant-side improvements. If branded TPV growth re-accelerates from 1% back to mid-single digits — even just halfway back — the multiple re-rates. You won’t see this in Q1; you might see early signs in Q2 or Q3. 4. Continued buyback execution. The boring catalyst, but the most reliable one. Every quarter that produces another $1.5B in buybacks at sub-$55 prices is a quarter where the math compounds quietly in your favor. Management has guided to $6B for 2026 and has $15+ billion of authorization remaining. The asymmetry is the point. To lose meaningfully from here, you need branded checkout to actively decline (not just decelerate), the buyback to be cancelled, and Venmo/BNPL/merchant services to all stall. That’s possible, but it requires several bad things to happen simultaneously to a business still generating $6B in annual cash, with a new CEO whose entire $25-62M upside depends on the stock at least getting back to its 2024 levels. The risks worth respectingI want to be fair to the bear case, because the bears have been right for five years.

The honest version of this thesis is: I don’t know whether branded checkout reaccelerates. Nobody does, including Lores on day one. But I don’t need to know, because the buyback gives me time to find out — and the new management is being paid in a way that makes their interests indistinguishable from mine. Bottom linePayPal at 9x earnings — with a 13% FCF yield, retiring 13% of its shares annually, sitting on a net-cash balance sheet, with a respected operator just installed as CEO whose entire $25-62 million upside is gated on the stock recovering — is the kind of setup value investors wait years for. It’s cheap because the business has real problems. It’s investable because the capital allocation works regardless of whether those problems get fully fixed, and because the people running it now are paid only to fix them. The market is pricing in continued decline. The buyback is pricing in survival. The CEO comp package is pricing in a double. I think survival is a low bar to clear. The rest is upside. Disclosure: This is a newsletter, not investment advice. Do your own work. Numbers are pulled from PayPal’s most recent SEC filings (8-Ks, 10-K, DEF 14A proxy), earnings releases through Q4 2025, the offer letter for Enrique Lores filed February 2026, and analyst commentary as of late April 2026. Stock prices, share counts, and authorization balances move; verify before acting. I may or may not own PYPL — disclose your own position before publishing. You're currently a free subscriber to Cheap Software Stocks. For the full experience, upgrade your subscription.

|