$META: Fire Sale or Value Trap?

$META: Fire Sale or Value Trap?The stock is down 32% from its all-time high. Two jury verdicts landed in a week. Capex is about to double to $135 billion. Here is everything you need to know before you decide.What Is Actually Happening to the StockMeta Platforms hit an all-time high of roughly $796 per share last August. Today it trades around $530, a drawdown of more than 32 percent. The Magnificent Seven narrative that carried it to those heights has fractured under the weight of three simultaneous pressures: a historic surge in capital expenditure, a string of legal defeats, and a broader macro environment rattled by tariffs and Iran tensions. The most immediate catalyst was a brutal week in the courtroom. On March 25, a Los Angeles jury found Meta and Google liable for social media addiction, ordering Meta to pay 70 percent of a $6 million award. The following day, Meta’s stock was down more than 11 percent for the week, the worst drop in the Magnificent Seven cohort that week. The day before the LA verdict, a New Mexico jury ordered Meta to pay $375 million for failing to protect children from predators on its platforms. Two adverse verdicts in 48 hours will do that to a stock. Compounding the legal pain, Meta announced in January that its 2026 capital expenditure guidance is $115 to $135 billion, nearly double the $72 billion spent in 2025. Investors who had grown accustomed to the margin expansion story of the “Year of Efficiency” suddenly found themselves staring at a company spending more on infrastructure in a single year than the entire 2022 market cap of many S&P 500 members.

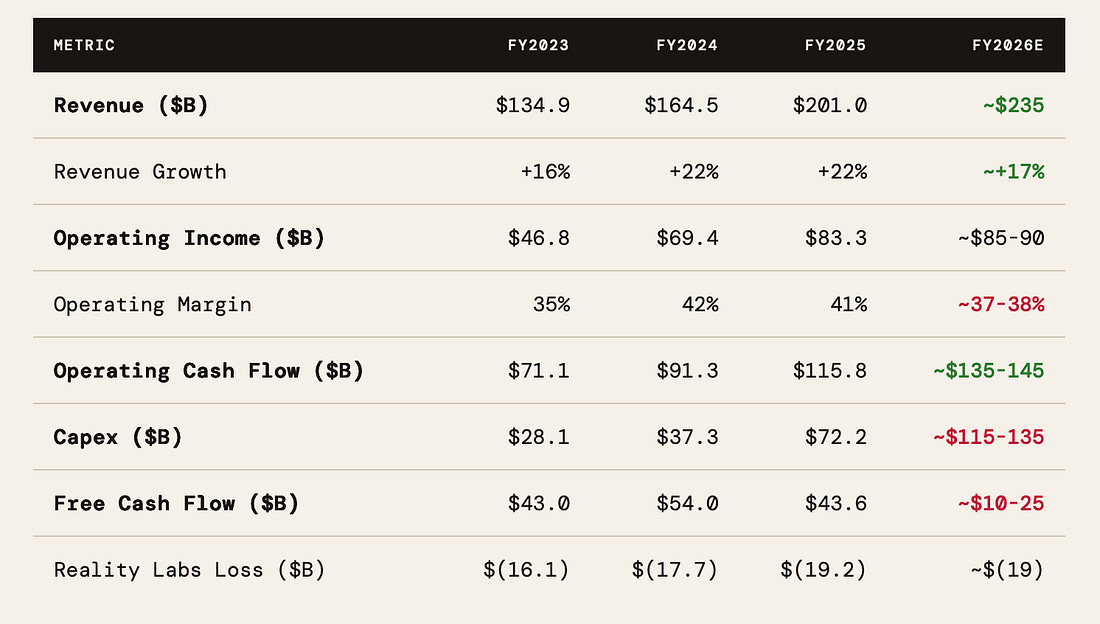

Then there is the macro backdrop. Trump’s tariff regime has weighed on advertising budgets, raised recession fears, and triggered a tech-wide sell-off. Meta fell 31 percent during the 2025 tariff shock, versus a 19 percent decline for the broader market. With a beta of 1.28, Meta reliably amplifies both market rallies and drawdowns. The Business: What Meta Actually DoesStrip away the headlines and Meta is one of the most structurally dominant advertising businesses ever assembled. The company operates in two segments: Family of Apps (FoA) and Reality Labs. The Family of Apps — Facebook, Instagram, WhatsApp, Messenger, Threads, and Reels — generated essentially all of the company’s $201 billion in revenue in 2025. Advertising is 97 percent of that total. Family daily active people reached 3.48 billion in Q2 2025, up 6 percent year over year, and hit 3.58 billion by Q4. For reference, that is roughly 44 percent of the entire human population engaging with a Meta product every single day. The advertising engine runs on two levers: impressions and price per impression. In Q4 2025, ad impressions grew while average price per ad rose 6 percent. The AI-driven Advantage+ ad suite has been meaningfully improving return on ad spend for advertisers, which in turn allows Meta to charge more. This is the compound loop that drives the business: more users leads to more data, which leads to better AI targeting, which leads to higher advertiser ROI, which leads to higher prices and more impressions. WhatsApp monetization remains the most underappreciated element of the Meta story. With over 3 billion monthly active users, WhatsApp is barely monetized today. Business messaging and click-to-WhatsApp ads are growing rapidly and could represent a multi-tens-of-billions annual revenue stream on their own. Reality Labs lost $19.2 billion in 2025 on revenue of roughly $2.3 billion, pushing cumulative losses past $75 billion since 2020. The segment has been a source of investor frustration for years. However, the narrative is beginning to evolve: Ray-Ban Meta smart glasses sales tripled year-over-year in the first half of 2025. The $799 Ray-Ban Display, which launched in September 2025 and sold out within 48 hours, suggests the wearables thesis is real. Zuckerberg said on the Q4 call that 2026 will likely represent peak Reality Labs losses as the company gradually reduces deficits going forward. True Cash Flows: Cutting Through the Capex FogThe headline free cash flow number of $43.6 billion for 2025 looks impressive. But it needs context. The $115-135 billion capex guidance for 2026 represents a near-doubling of the $72 billion spent in 2025. If operating cash flow grows at roughly 20 percent and hits around $140 billion in 2026, and capex lands at the midpoint of $125 billion, free cash flow would compress to approximately $15 billion — a drop of more than 65 percent year over year. This is the number that should terrify investors in the near term and excite them in the medium term. The compression is real and front-loaded. But capex is not consumed the moment it is spent; it gets depreciated over 10-15 years for data centers and 3-5 years for servers. The cash is spent now; the expense hits the income statement slowly. The gap between cash capex and depreciation is what Wall Street calls “capex overhang,” and Meta is sitting on a massive one.

There is also the joint venture structure to understand. Meta entered a $27 billion joint venture with Blue Owl Capital for its Hyperion data center in Louisiana, with Blue Owl covering 80 percent of the cost. This off-balance-sheet structure reduces the direct cash burden somewhat. Similarly, the $100 billion agreement with AMD and the CoreWeave cloud deal spread some infrastructure costs to operating expenses rather than pure capex. The true economic capex picture is complex, but the cash demand is undeniably large. Looking at maintenance versus growth capex matters here. Meta’s baseline infrastructure to support the current ad business probably requires $20-30 billion annually. Everything above that is discretionary AI investment — a bet on future revenue streams that do not yet exist at scale. Investors are effectively paying for a $100 billion per year AI lottery ticket, with a mature advertising business as the collateral.

The AI Bet: What Are They Actually BuildingMeta’s AI strategy has undergone a significant pivot. The company spent years as the champion of open-source AI through its Llama model family, building enormous goodwill with the developer community. That era appears to be ending. After a lukewarm reception to Llama 4 and growing concern that DeepSeek had incorporated elements of Llama’s architecture, Meta is now developing a closed-source successor codenamed Avocado. The strategic reorganization is equally notable. In July 2025, Zuckerberg launched Meta Superintelligence Labs (MSL), consolidating all AI research under a single banner with the explicit goal of building superintelligence. MSL is led by Alexandr Wang, who joined as part of a $15 billion acquisition of Scale AI. Meta has reportedly offered signing bonuses of up to $1 billion to recruit top researchers. Yann LeCun, the longtime chief AI scientist and “godfather of AI,” departed in late 2025 amid the strategic shift away from open-source. Two flagship models are in development. Mango is a multimodal image and video generation model. Avocado is a reasoning-focused LLM targeting strong coding performance. Both were originally scheduled for a first-half 2026 internal release, though Avocado encountered training challenges that pushed it back. The AI infrastructure buildout is staggering. Meta committed to spending $600 billion on U.S. infrastructure through 2028. The Hyperion data center in Louisiana is projected to eventually scale to 5 gigawatts. The Prometheus data center in Ohio is expected to be online in 2026. Meta signed a $100 billion multi-year deal with AMD for GPU infrastructure, a $27 billion compute deal with Nebius Group, a $14.2 billion deal with CoreWeave, and is reportedly in talks with Oracle for another $20 billion agreement. The core thesis is that Meta’s 3.58 billion daily active users represent the world’s most valuable distribution platform for AI products. Meta AI, the assistant embedded across Facebook, Instagram, WhatsApp, and Messenger, has a built-in audience that no standalone AI company can match. If Avocado performs at the frontier level and Meta AI becomes genuinely useful, the monetization runway expands from advertising alone into AI services, premium subscriptions, and enterprise tools.

Lawsuit Risk: The Legal IcebergThe legal exposure facing Meta in 2026 is broad, complex, and genuinely material. Three distinct litigation vectors deserve attention. The FTC Antitrust CaseThe longest-running legal threat reached a significant turning point in November 2025 when U.S. District Judge James Boasberg ruled that Meta does not hold monopoly power in personal social networking, given competition from TikTok and YouTube. The court’s analysis focused on current market conditions rather than the state of the market in 2012 and 2014 when Meta acquired Instagram and WhatsApp, respectively. However, the FTC filed an appeal in January 2026 and the case continues. Even if the FTC wins on appeal, legal experts note that proving current competitive harm is a steep climb. The government still needs to demonstrate that Meta’s conduct is harming competition in 2026, not just relitigate acquisitions from a decade ago. The structural risk of forced divestiture of Instagram or WhatsApp is the tail risk that matters — low probability but existential in impact. Youth Addiction and Harm LitigationThis is the more immediate and potentially more damaging legal frontier. The recent California and New Mexico verdicts are bellwether cases in what could become Big Tech’s tobacco moment. As of March 2026, more than 235 plaintiffs are in federal multidistrict litigation against Meta, over 250 school districts have filed suits, and more than 100,000 individual mass arbitration claims have been submitted. The design-defect legal theory — targeting platform architecture rather than user-generated content — sidesteps Section 230 protections in a way that could unlock enormous liability. The individual damage awards so far are immaterial ($375 million in New Mexico, a few million in California). But the precedent is the point. Analysts estimate total industry-wide legal exposure at $10 to $50 billion depending on how appellate courts treat the design-defect theory. Meta has already warned in its 2026 10-K that youth addiction lawsuits and mass arbitration “could significantly impact” financial results. The tobacco parallel is imperfect but instructive: the industry settled for $246 billion spread over 25 years. A similar settlement trajectory for Big Social would be painful but survivable for a company generating $140 billion in operating cash flow. European and Global RegulationThe EU AI Act imposes transparency obligations on Meta’s agentic tools. The Digital Markets Act creates interoperability requirements for dominant platforms. GDPR fines continue to accumulate. Meta has introduced location-based fees for European advertisers to offset compliance costs. European regulatory friction is a chronic drag rather than an acute risk, but it limits Meta’s ability to extract maximum value from its European user base.

Growth Trajectory: Where Is This Business GoingMeta’s revenue grew 22 percent in 2025, powered by AI-enhanced advertising and continued user growth. Q4 growth accelerated to 24 percent. Management guided Q1 2026 revenue of $53.5-56.5 billion, implying approximately 28-33 percent year-over-year growth at the midpoint — an acceleration. Consensus analyst estimates project 2026 revenue around $235-240 billion, implying roughly 17-19 percent growth. The digital advertising market is Meta’s primary growth driver. AI-powered ad targeting through tools like Advantage+ has increased advertiser ROI, allowing Meta to raise effective CPMs. In Q4 2025, average price per ad grew 6 percent while ad impressions also grew — volume and price moving together is the dream scenario for an ad business. Three incremental revenue vectors are worth tracking. First, WhatsApp monetization remains nascent. Click-to-WhatsApp advertising and business messaging APIs are growing fast from a small base. Second, Threads has scaled to hundreds of millions of users with minimal monetization so far; early ad tests have been promising. Third, AI Services — a premium Meta AI tier or enterprise Llama licensing — represents blue-sky upside that is not yet in any model. Consensus growth forecasts call for roughly 15-20 percent revenue CAGR over the next three years. That implies revenues approaching $300-350 billion by 2028. If margins recover as capex normalizes, the earnings power of this business in 2028-2030 could be extraordinary. DCF Valuation: What Is It Actually WorthBuilding a DCF for Meta requires making honest assumptions about the capex trough, the revenue growth rate, and the terminal margin. Here is a grounded framework using three scenarios. Key Assumptions for All ScenariosCurrent price: approximately $530. Shares outstanding: approximately 2.53 billion. Discount rate: 10 percent (reflecting Meta’s market beta and risk profile). Terminal growth rate: 3.5 percent. The FY2026 FCF trough is painful but temporary; the question is the recovery trajectory.

Applying a DCF with a 10 percent discount rate and these terminal values, discounted back to today:

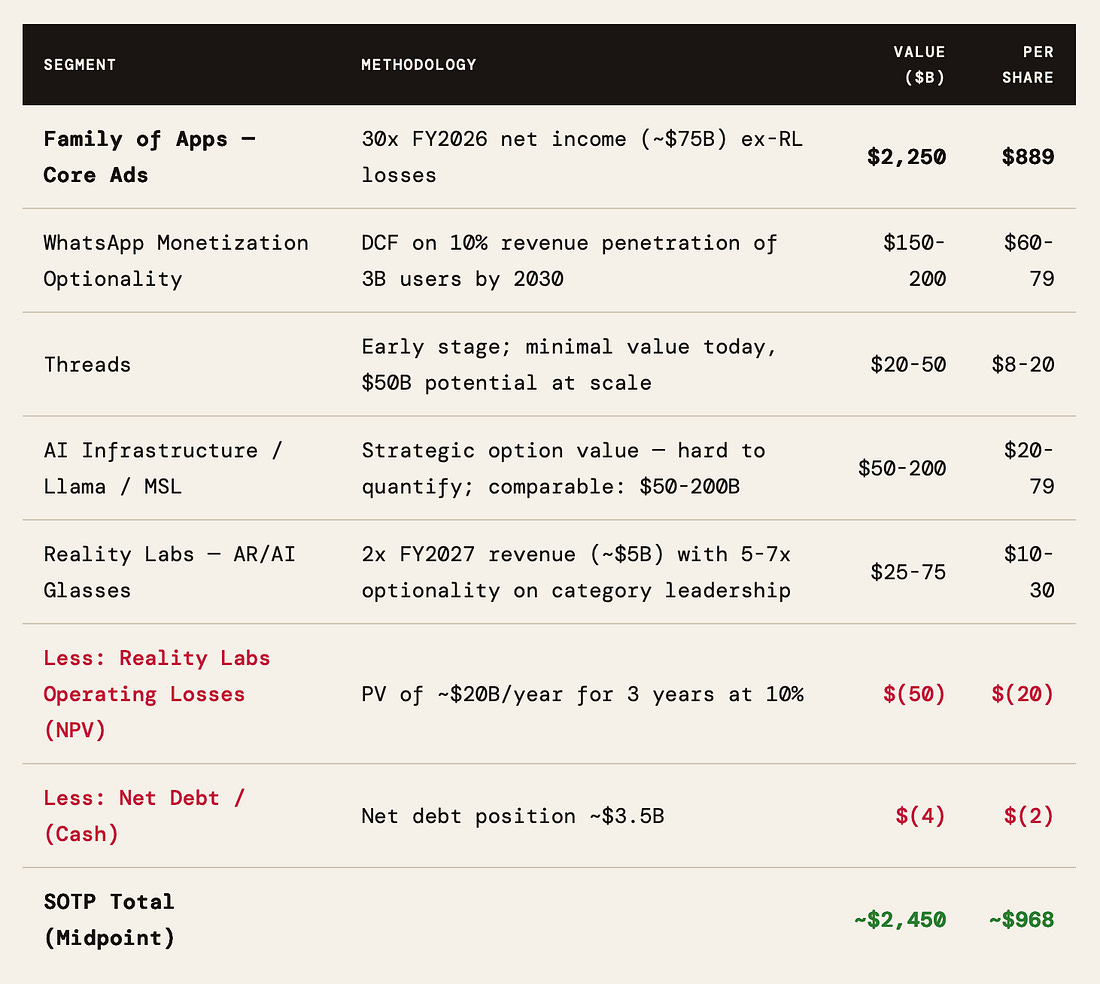

The base case is $730, implying roughly 38 percent upside from current levels. The wide dispersion between bear and bull reflects genuine uncertainty about whether the capex spending generates returns. The consensus analyst target is around $840-875, suggesting Wall Street is pricing something between the base and bull. The average 1-year price target across Wall Street is $873, with a high of $1,200 and a low of $683. Sum of the Parts: Breaking the Business ApartValuing Meta as a monolith misses the texture of what is inside. A sum-of-the-parts analysis reveals both the value buried in the core advertising business and the optionality embedded in Reality Labs and AI infrastructure.

The SOTP analysis is instructive but comes with important caveats. The 30x multiple on the core ad business feels defensible for a franchise growing 17-22 percent with 82 percent gross margins and near-monopoly positioning in social advertising. The optionality values on WhatsApp, AI, and glasses are speculative by nature. The key takeaway is that even if you assign zero value to everything except the core advertising business and apply a conservative 25x multiple on FY2026 earnings, you get to roughly $700-750 per share — comfortably above today's price. The Fears: What Could Actually Break ThisThe bears have a real case. It centers on several scenarios that should not be dismissed. The first and most plausible bear case is that the $125 billion in annual capex does not translate into meaningful new revenue streams for four to five years, during which time free cash flow remains suppressed, earnings multiples compress further, and investor patience runs out. This is the “Amazon in 2014” scenario — and it is worth noting that Amazon’s stock went nowhere for years before the AWS flywheel became undeniable. The second fear is AI model irrelevance. Llama 4 was widely considered a disappointment relative to models from OpenAI, Google, and Anthropic. If Avocado also fails to achieve frontier performance, Meta risks spending $600 billion building the world’s most expensive second-tier AI infrastructure. Developer adoption of Meta’s models reportedly declined significantly following the open-source pivot uncertainty. Without a competitive model, the AI assistant and AI services strategies become difficult to execute. The third fear is advertising cyclicality. Digital advertising is not recession-proof. If tariffs tip the U.S. economy into a meaningful slowdown in 2026, advertiser budgets will be cut. Meta’s entire operating leverage thesis depends on advertising continuing to compound at double-digit rates. A recession that cuts advertising growth to low single digits while capex stays at $125 billion would be genuinely painful. The fourth fear is legal and regulatory in nature. The youth addiction litigation, if it reaches a Big Tobacco-scale settlement, could impose both financial costs and platform redesign mandates. If courts require Meta to fundamentally alter the engagement-optimization algorithms that make Instagram and Facebook so effective at retaining users, the advertising business model is impaired at its foundation. The fifth fear is that TikTok returns to the U.S. market fully. Meta benefited enormously from TikTok’s near-banishment. Reels user growth, advertiser migration, and engagement metrics all reflected the reduced competitive pressure. If TikTok returns at full strength, some of that accreted value reverses. Current Valuation and the SetupMeta currently trades at roughly 25x trailing earnings and 19.7x forward earnings, with a PEG ratio of 0.88 — below 1, which conventionally suggests undervaluation relative to growth. The current P/E of approximately 22x is 22 percent below Meta’s 10-year historical average of 28x. The stock has a 52-week high of $794 and a 52-week low of $478. The average analyst price target is around $844, implying roughly 60 percent upside from the current price. The forward multiple compression tells an interesting story. At $530 and with consensus 2026 EPS estimates around $29, the stock is trading at roughly 18x forward earnings. For a company growing revenue at 17-20 percent with 82 percent gross margins, a 18-19x forward multiple is genuinely inexpensive relative to history. The compression reflects the FCF trough from elevated capex, not a deterioration in the underlying business quality. GuruFocus rates Meta’s GF Value at $754, calling the stock modestly undervalued with a GF Score of 99 out of 100. The EV/EBITDA of approximately 13.6x is also below what you would expect for a business with this growth profile and margin structure. The stock repurchase program adds a floor element. In 2025, Meta spent $26.3 billion on buybacks and paid $5.3 billion in dividends. Share count declined 1.53 percent over the past year. Even with the FCF trough in 2026, Meta has $81.6 billion in cash and securities to deploy. Buybacks at current levels represent a meaningful yield on top of the fundamental growth. The Setup: How to Think About Owning ThisMeta in 2026 is a story of temporary cash flow pain in service of potentially permanent competitive advantage. The question every investor must answer is whether they believe: (1) the advertising business keeps growing at 15-20 percent; (2) the AI infrastructure eventually generates a return; and (3) the legal risks are manageable and not structurally impairing to the business model. If you believe all three, the stock at roughly 19x forward earnings is arguably cheap. If you believe any of the three fails, the downside to the $350 bear case is material from here. The setup has some characteristics that are genuinely interesting for patient capital. The capex cycle is well understood and widely feared, which means its peak is increasingly priced in. The legal verdicts this week caused the stock to sell off sharply, but the actual dollar amounts ($375 million in New Mexico, a few million in California) are rounding errors on a $43 billion free cash flow business. The market’s reaction appears to be pricing in the precedent risk, not just the specific damages. If appeals modify those precedents, there is sentiment upside. The position sizing question matters. Meta’s beta of 1.28 means it amplifies market moves in both directions. In a macro environment with active Iran tensions, tariff uncertainty, and a Fed that may cut rates unevenly, that amplification cuts both ways. Averaging into a position over the next few quarters rather than committing a full allocation today would allow an investor to benefit from continued weakness while not missing a potential sharp recovery if the April 29 earnings call is clean.

The Bottom LineMeta Platforms is a business generating $201 billion in annual revenue, growing at 22 percent, with 82 percent gross margins and 3.58 billion daily active users. Its core advertising engine is being strengthened by AI. Its next platform — AI glasses — is showing genuine commercial traction. Its management team has demonstrated, most recently in 2023’s “Year of Efficiency,” a willingness to make hard decisions and execute. The risks are real. The capex is genuinely enormous. The legal exposure is broad and uncertain. The AI model competition is fierce. The macro environment is hostile to high-multiple growth stocks. But at 19x forward earnings with a PEG below 1, the stock is pricing in a lot of bad news. Our base case DCF yields $730, roughly 38 percent upside. A full sum-of-the-parts analysis puts fair value closer to $968. Wall Street consensus is $844. The setup is for patient investors willing to live through a year of compressed free cash flow in exchange for optionality on one of the most consequential AI buildouts in corporate history. This is not a trade. It is a 2-3 year thesis that requires conviction in the advertising business’s durability and at least some belief in the AI return on investment. Those who hold it with that time horizon have historically been rewarded. Those who need quarterly FCF validation will find the next few quarters uncomfortable. Cheap Software Stocks is free today. But if you enjoyed this post, you can tell Cheap Software Stocks that their writing is valuable by pledging a future subscription. You won't be charged unless they enable payments.

|